Introduction

The National Higher Education Fund Corporation (PTPTN) continuously strives to ensure the sustainability of education loan funds for the benefit of future generations. However, the low repayment rate from some borrowers raises concerns about PTPTN's financial sustainability.

To date, a significant number of borrowers have been identified as failing to settle their education loan debts, especially those with arrears exceeding 10 years. PTPTN has made various efforts to help them repay their overdue loans without causing financial strain, yet many still fail to come forward for consultation. If this situation is not addressed promptly, it will have long-term effects on future generations, the higher education system, and the development of the nation's human capital.

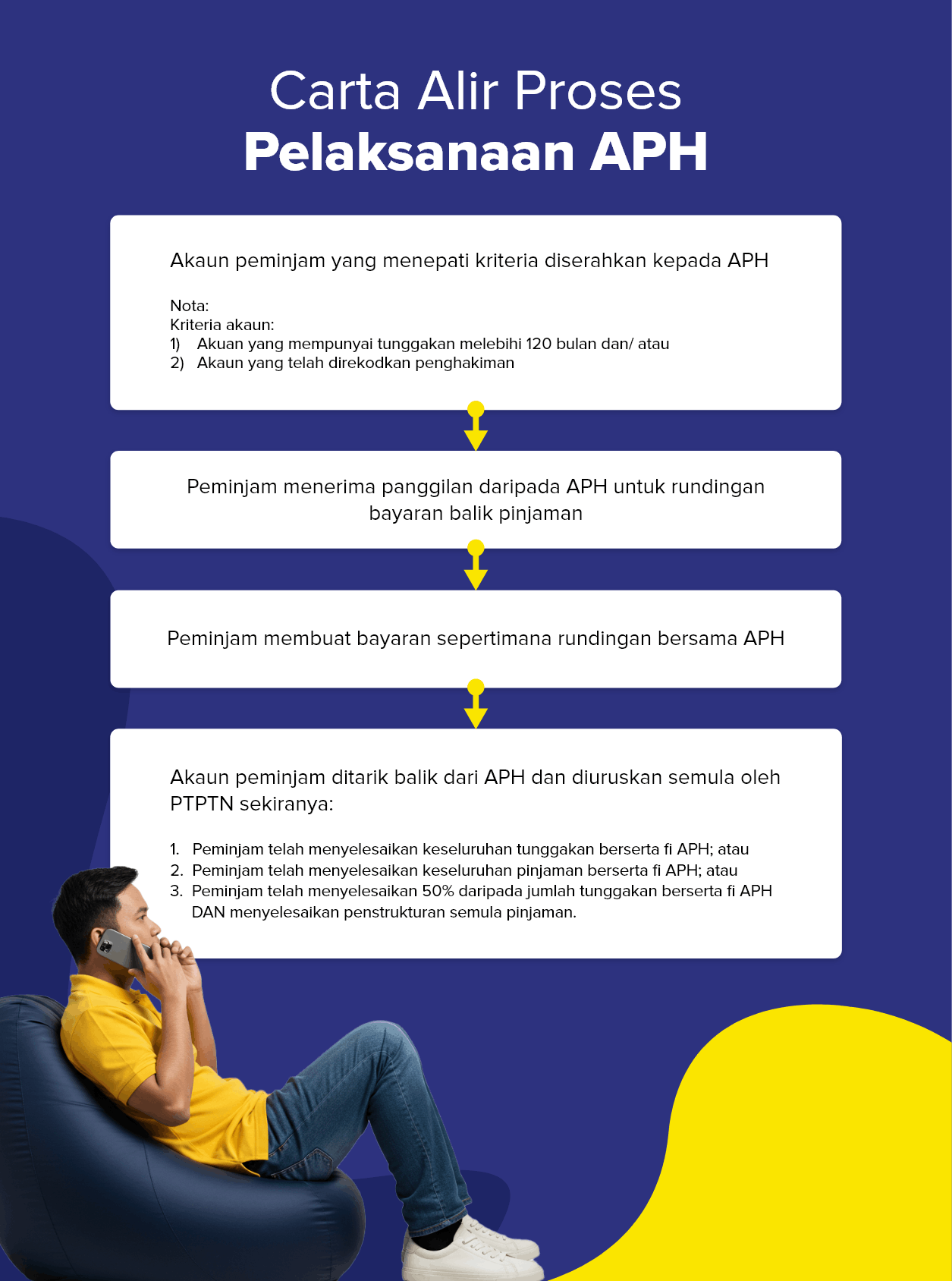

Accordingly, PTPTN has engaged the services of Debt Consulting Agencies (APH) as one of its strategic measures to address the issue of chronic loan defaulters. This service will involve borrowers with arrears exceeding 120 months and/or those against whom a judgment has been recorded by the Court. This initiative is in line with the Government’s aspiration to strengthen the collection of PTPTN education loan repayments.

Contents

Appointment of the APH

PTPTN places great importance on the security of information and the rights of borrowers. The appointment of APH is based on Section 35 of the PTPTN Act 1997 (Act 566), which grants PTPTN the authority to appoint any agent, consultant, or individual to carry out related tasks or functions, including debt collection.

Agencies appointed as PTPTN Debt Consulting Agencies will be provided with a letter of appointment and/or letter of authorisation as official identification when carrying out their duties. The following is the list of APHs officially appointed by PTPTN:

- PASADANA SDN. BHD.

- RURAL CAPITAL BERHAD

- MAYSKY (M) SDN. BHD.

- CHAIN RESOURCES (M) SDN. BHD.

If a borrower receives a call or is contacted by someone claiming to be a representative of APH, they are advised to verify the identity of that individual. If there is any doubt, borrowers can contact the PTPTN Careline at 03-2193 3000 or Live Chat on the PTPTN Portal to make a verification or lodge a complaint.

Submission of Borrower Information to the APH

Borrower accounts that meet the prescribed criteria will be referred to APH for the purpose of loan repayment negotiation. Once the account has been referred, all account management matters, including those related to the borrower’s loan repayment negotiation, will be handled entirely through APH, and the borrower will no longer be allowed to negotiate directly with PTPTN.

Imposition of Service Fees & Loan Restructuring

Each payment collected by APH will be subject to a fee of 15% of the amount successfully collected, and the fee shall be fully borne by the borrower.

Loan restructuring is only allowed once the borrower has successfully settled at least 50% of the total outstanding arrears together with the APH fee. The borrower is required to submit a loan restructuring application and complete all restructuring processes, including returning the duly completed agreement documents via myPTPTN. Thereafter, the borrower’s account will be removed from APH and managed by PTPTN again.

Official Channels for Loan Repayment

All loan repayments must be made only through PTPTN’s official payment channels. For more accurate, faster and secure transactions, borrowers are encouraged to make repayments via myPTPTN.

APH is not allowed to receive any cash payments from borrowers. Once payment has been made, borrowers must submit proof of payment to APH for verification and record purposes.

Flow Chart of the APH Implementation Process

This flow chart is provided to help borrowers better understand each step involved, offering a clearer overview of the APH implementation process carried out by PTPTN.

Conclusion

The implementation of APH by PTPTN is a firm and structured initiative to address the issue of defaulting borrowers, which affects the national education financing system. Through this appointment, PTPTN aims to enhance the effectiveness of loan collection in a professional manner without neglecting the welfare of borrowers.

Therefore, borrowers are advised to take proactive action at all times in making loan repayments or to contact PTPTN for negotiation to prevent their loan accounts from being referred to APH. The commitment to repay loans is not merely a legal obligation, but also a moral responsibility towards the future of education for generations to come.